CannTrust Holdings’ (CSE:TRST) emergence as a leading player in Canada’s medical cannabis market has enabled it to achieve a market capitalization north of $600mln since debuting on the Canadian Securities Exchange on August 21 of this year.

As impressive as that is, Canada’s plan to legalize recreational use of the drug, widely expected in July 2018, clearly has the potential to take the company to even greater heights.

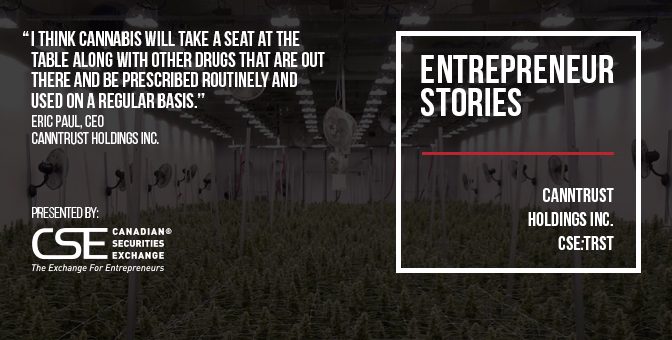

The licensed producer acquired a 430,000 sq. ft. greenhouse in Niagara, Ontario and has completed a first phase, state-of-the-art renovation of 250,000 sq. ft. that is now in production.

The second phase of 180,000 sq. ft. will be finished by March 2018, and with 430,000 sq. ft. in production the conservative estimate for annual output is 40,000kg of cannabis.

Late 2018 should see an additional expansion of 600,000 sq. ft. on the 46-acre site to meet anticipated growth in demand from medical and recreational users.

A larger long term player…

Chief Executive Officer Eric Paul explains this will cement CannTrust’s position as one of the larger “longer term players” in the Canadian cannabis market. As it is, the company is already firmly in the top 10.

Canada is one of a handful of countries where medical cannabis is legal, and permitting recreational use will not only fulfill an election promise by Prime Minister Justin Trudeau, but also means it will become the first major industrialized nation with a system permitting both uses.

Paul is bullish on the potential for the recreational market, pointing to projected numbers from groups, including Health Canada, which put its size above $5bln annually.

In terms of users, the medical market is estimated to reach 450,000 to 500,000 people, and the recreational market is projected to be three to five times the size of the medical market, Paul notes.

“Anyone who’s buying in now (to CannTrust) – because they are buying into a company that’s well-structured and has the physical assets to grow high quality product at the right cost structure – is going to win,” suggests Paul.

“I think cannabis will take a seat at the table along with all the other drugs that are out there and be prescribed routinely and used on a regular basis.”

Founded in 2013..

CannTrust was founded in 2013 with a view to getting a license under the Access to Cannabis for Medical Purposes Regulations (ACMPR) framework, which it accomplished early in 2014.

It started selling product in 2015 via mail based on physician’s prescriptions and now boasts a “menu” for customers of around 12 high quality products, including oils.

These can be used for symptoms ranging from pain to stress to sleeplessness and auto-immune conditions.

The company went public in August of this year, when it was producing from an indoor hydroponic facility with annual capacity for 2,500kg of cannabis.

The shift to a large new greenhouse taking advantage of natural light allows CannTrust to increase output and reduce operating costs, explains Paul.

Taking production to 1mln sq. ft. once the full expansion plan has been implemented should make CannTrust one of the top three Canadian producers.

An expanding customer base..

Paul says the CannTrust customer base has expanded 117% since May to 32,500 active patients, positioning it among the fastest growing players in the industry.

In addition, its greenhouse approach allows CannTrust to produce cannabis for some 50% less than facilities completely dependent on artificial light. The reduction in costs from around $1.50 per gram to $0.75 can be expected to have a positive influence on margins.

The first phase greenhouse expansion has already been funded and a recent $20mln placement will pay for the second phase, as well as some ancillary improvements to supply channels.

Interestingly, Paul thinks the market that observers refer to as “recreational” is actually being mislabeled.

“We don’t believe that everyone out there is just the sort of person who wants to get high at the weekend. We’re postulating that two thirds of the recreational market is a person over 30 who’s chronically ill and self-medicating,” he says.

With revenue rising quickly, Paul expects the company to be profitable in the 2017 financial year. Analysts see the potential as well.

Analysts upbeat..

Haywood Securities recently began covering the stock with a ‘Buy’ rating and target price of $8.00.

“CannTrust reported Q3/17 growth of 35%, resulting in revenues of $6.1 million. Importantly, the company also announced that 61% of its sales were from oil products that drive higher margin sales,” said Haywood.

“We believe that CannTrust’s % of sales of oil/extract products will continue to increase, particularly as it releases new products, such as capsules it is currently working on, but other novel products that are likely to be developed through its partnership with Apotex (private).”

The broker predicts EBITDA of $5mln on revenues of $20.7mln for 2017.

Canaccord initiated coverage in October with a ‘Speculative Buy’. “Based on the company’s low-cost production, leading growth profile, and forecast superior margins (driven by its medical strategy), we believe that CannTrust deserves to trade at a premium multiple to peers,” Canaccord stated.

The company’s performance on the CSE has proven the analysts right, with its share price recently cresting $7.50, up some 200% from its August debut.

It is quite a story, but with regulatory change on the horizon and production set to rise several fold, CannTrust looks to just be getting started.

This story was originally published at www.proactiveinvestors.com on December 5, 2017 and featured in The CSE Quarterly.Learn more about CannTrust Holdings at http://www.canntrust.ca/ and on the CSE website at http://thecse.com/en/listings/life-sciences/canntrust-holdings-inc.